Financial institutions face strict mandates. Specifically, Basel III, the EBA, and the European Central Bank (ECB) require rigorous stress tests. These tests focus on non-maturity deposit (NMD) portfolios. However, a primary challenge exists. Accurately modeling deposit outflow rates is difficult. This is true across diverse, low-probability stress scenarios. For instance, idiosyncratic reputation shocks or widespread market failures.

Furthermore, preserving complex dependencies is hard. These include client type, transaction history, and macroeconomic factors. Northhaven Analytics addresses this critical regulatory gap. To do so, we deliver an institution-specific synthetic data generator.

In short, this dedicated generative model replicates precise temporal dynamics. Moreover, it captures distributions and correlation structures of deposit balances. Consequently, the synthetic dataset provides unlimited, privacy-compliant data. This is necessary for validating internal Liquidity Risk Models (LRMs). Additionally, it enables exhaustive, counterfactual Liquidity Risk Stress Testing (LRS) at scale. Ultimately, this strengthens regulatory compliance and minimizes Model Risk.

Problem Definition: Liquidity Risk & Deposit Dynamics

Accurate modelling of deposit stability is paramount. Specifically, it is vital for meeting regulatory metrics. These include the Liquidity Coverage Ratio (LCR) and Net Stable Funding Ratio (NSFR). However, Treasury, Risk, and Model Validation functions face a core problem. This stems from the inherent nature of deposit data.

Complexity of Non-Maturity Deposit (NMD) Behaviour

NMD behaviour is driven by opaque client psychology. Moreover, it is highly conditional on external and internal events. The decision to withdraw funds is a complex sequence. Specifically, this „deposit outflow” is temporal. It depends on variables such as recent transactional activity and average balance tenure. Furthermore, the size of the deposit and relationship history matter. Finally, all this is modulated by market sentiment.

Regulatory Requirement for Extreme Scenarios

Supervisory expectations are high. For instance, the ECB requires LRMs to be stress-tested against extreme scenarios. These scenarios must far exceed historical observations. However, real historical data is limited. It rarely contains sufficient instances of coordinated, severe outflow events. Yet, these are required to robustly calibrate model parameters. Therefore, validating the model’s performance at the tails of the outflow distribution is difficult with real data.

Intraday Liquidity Modeling

Advanced compliance requirements exist. Specifically, they necessitate modeling intraday liquidity fluctuations. This requires high-frequency transactional data. However, this data is difficult and costly to aggregate. In addition, using it safely across compliance and risk departments is a challenge.

Data Constraint & Regulatory Gap

The reliance on real production data creates bottlenecks. Indeed, these are often unavoidable.

Model Risk (SR 11-7): Models are often validated using compromised data. As a result, the assessment of model uncertainty (MU) is flawed. This violates the spirit of SR 11-7 requirements. Ultimately, it creates unmitigated operational risk.

PII and Privacy Restrictions (GDPR): Deposit transaction history constitutes sensitive PII. Therefore, sharing this granular data is typically prohibited. Alternatively, it requires costly, complex anonymization. Unfortunately, this often destroys temporal fidelity. Read about our privacy-first approach in Why Northhaven Outperforms.

Data Sourcing Limitations: Accessing a unified dataset is challenging. Specifically, one that combines high-frequency transaction data with client master data is rare. Furthermore, adding macroeconomic indices and internal bank-specific events is difficult.

Scalability Issues: LRS requires Monte Carlo simulations. Consequently, models require millions or billions of observations. However, this scale is unreachable with real data. This is due to cost and governance friction.

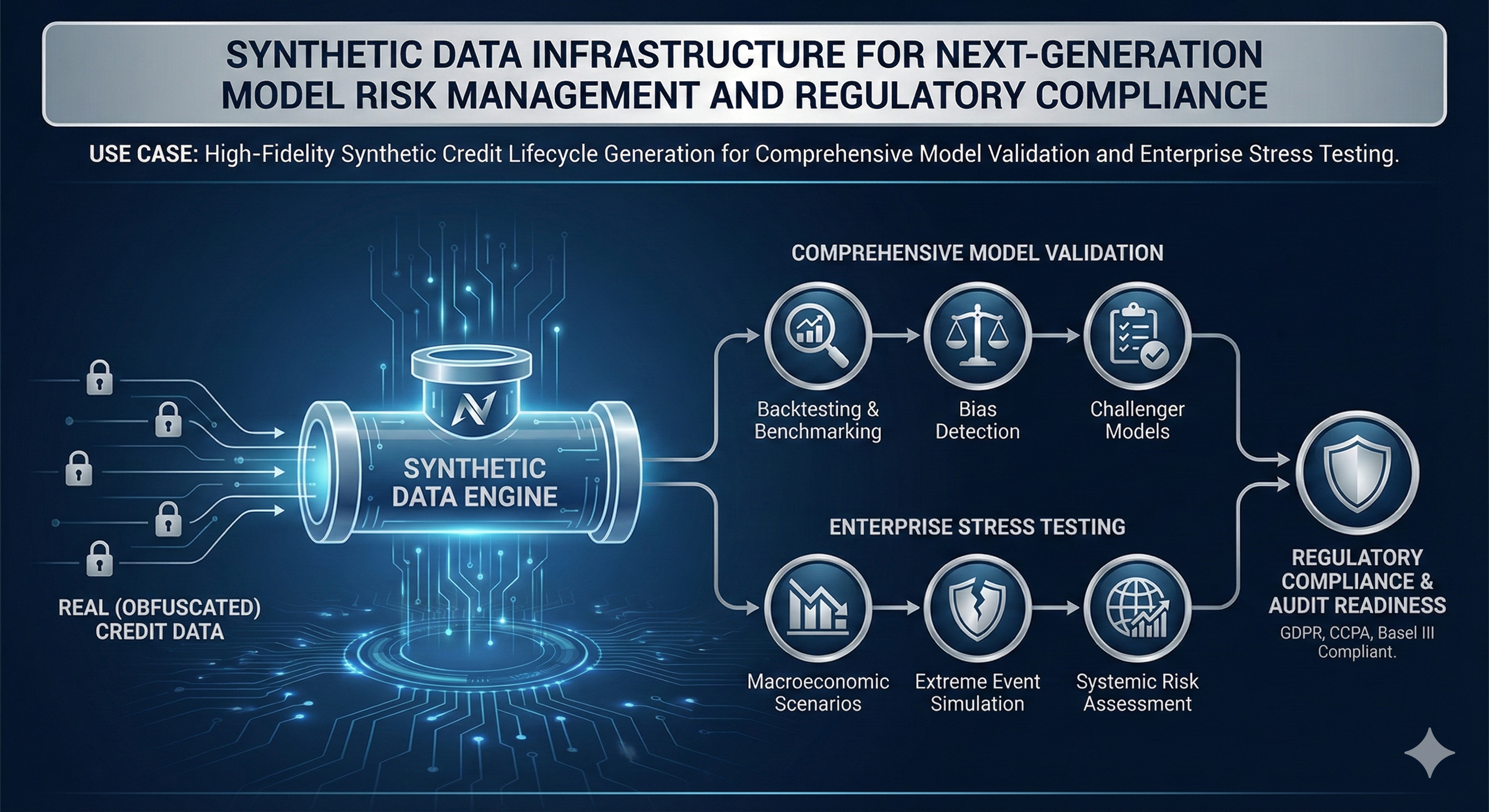

Northhaven Solution: Architecture and Fidelity

Northhaven Analytics deploys a dedicated, custom-trained Synthetic Deposit Behaviour Generator—a generative ML model designed exclusively to replicate the complex temporal and conditional characteristics of the client’s deposit base.

Generative Architecture: The solution leverages a sophisticated hierarchical probabilistic framework, combining elements of Conditional CTGAN (C-CTGAN) for modeling static client/account attributes and a Temporal Sequence Model (TSM)—such as a custom Recurrent Neural Network (RNN) or a Transformer-Discriminator—for generating realistic sequences of transactional events and resulting deposit balances over time.

- Client-Level Generation: The C-CTGAN module generates static account properties (e.g., account tenure, product mix, initial balance distribution) while preserving inter-feature correlations.

- Temporal Dynamics: The TSM is then conditioned on the static output to generate high-frequency sequences, ensuring that the simulated deposit outflows adhere to observed market factors and internal bank-specific logic (e.g., outflows are non-linear around large, predefined payment dates).

- Constraint Embedding: Critical regulatory constraints (e.g., total volume conservation, non-negative balance) and financial logic rules are embedded into the model’s loss function, ensuring the synthetic data maintains structural integrity.

Fidelity and Scale: The generative model is trained strictly on statistical aggregates and schema definitions, guaranteeing zero privacy leakage. Fidelity is quantitatively verified using:

- Time-Series Divergence Metrics: Assessing the statistical distance (e.g., Dynamic Time Warping or Wasserstein Distance for time series) between the synthetic and real deposit outflow curves under various stress conditions.

- Autocorrelation Function (ACF) Preservation: Ensuring the synthetic transactional data exhibits the same lag-based dependency structure as the real high-frequency data.

The generator can scale efficiently, delivering one million records in under six minutes for complex schemas, enabling the generation of a full synthetic deposit portfolio (up to 1 billion records) for comprehensive LRS simulations.

Regulatory Alignment & Model Governance

The Northhaven solution directly supports the institution’s commitment to robust Model Risk Management and regulatory compliance:

- SR 11-7 Validation: Provides the Model Validation function with unlimited, non-PII data for independent testing and benchmarking of LRMs against internal challenger models, addressing the use and outcome of the model validation process.

- EBA/ECB Liquidity Stress Testing: Enables the creation of statistically valid, counterfactual stress-test scenarios (e.g., simulating extreme deposit runs under simultaneous sovereign risk downgrades) that go beyond simple historical replication, thereby satisfying supervisory demands for robust tail-risk coverage.

- Auditability and Version Control: The use of the Northhaven platform includes robust documentation and versioning control, ensuring that every synthetic dataset used for a regulatory submission can be traced back to the exact generative model version, meeting governance standards for transparency.

Measurable Outcomes & Benefits

| Outcome Category | Benefit Description | Target Metric Improvement |

| Liquidity Risk Coverage | Full coverage of low-frequency, high-severity deposit outflow scenarios required by supervisors. | 100% of defined tail scenarios generated on-demand. |

| Validation Cycle Time | Elimination of internal legal/compliance delays related to data provisioning. | 60% reduction in data preparation time for LRM validation. |

| Model Calibration Accuracy | Improved calibration of LRM parameters (e.g., outflow ratios) due to exposure to realistic stress conditions. | Reduction of Model Uncertainty (MU) metrics by >15%. |

| Cost Efficiency | Elimination of costs associated with complex PII masking tools and external data procurement for benchmarking. | Significant reduction in data governance and processing costs. |

| Compliance Posture | Provides auditable proof of LRS scale and robustness using certified, non-PII data. | Strengthened regulatory assessment scores for LRS. |

Risks Mitigated by Synthetic Data

The Northhaven generator mitigates several systemic risks inherent in traditional liquidity risk workflows:

- Privacy Risk: Eliminates the risk of PII exposure when collaborating with external vendors or utilizing cloud-based analytical platforms.

- Model Drift: Reduces the risk of Model Drift or bias introduced by overly aggressive or incomplete data masking techniques, ensuring that the validation environment accurately reflects the production data’s statistical reality.

- Capital Risk: Improved model robustness leads to lower Model Uncertainty (MU), potentially reducing required capital add-ons imposed by supervisory bodies.

- Scenario Blindness: Mitigates the risk of failing to predict extreme but plausible liquidity events due to the scarcity of relevant historical data.

Key Takeaways

- Focus: Synthetic data is the essential enabler. Specifically, for validating complex Liquidity Risk Models.

- Deliverable: Northhaven provides a dedicated generative ML model.

- Impact: It enables the safe generation of up to 1 billion records.

- Uniqueness: The solution guarantees high-fidelity replication. Simultaneously, it maintains zero privacy leakage.

- Contact Us to Discuss Liquidity Risk