By Northhaven Analytics Research Team

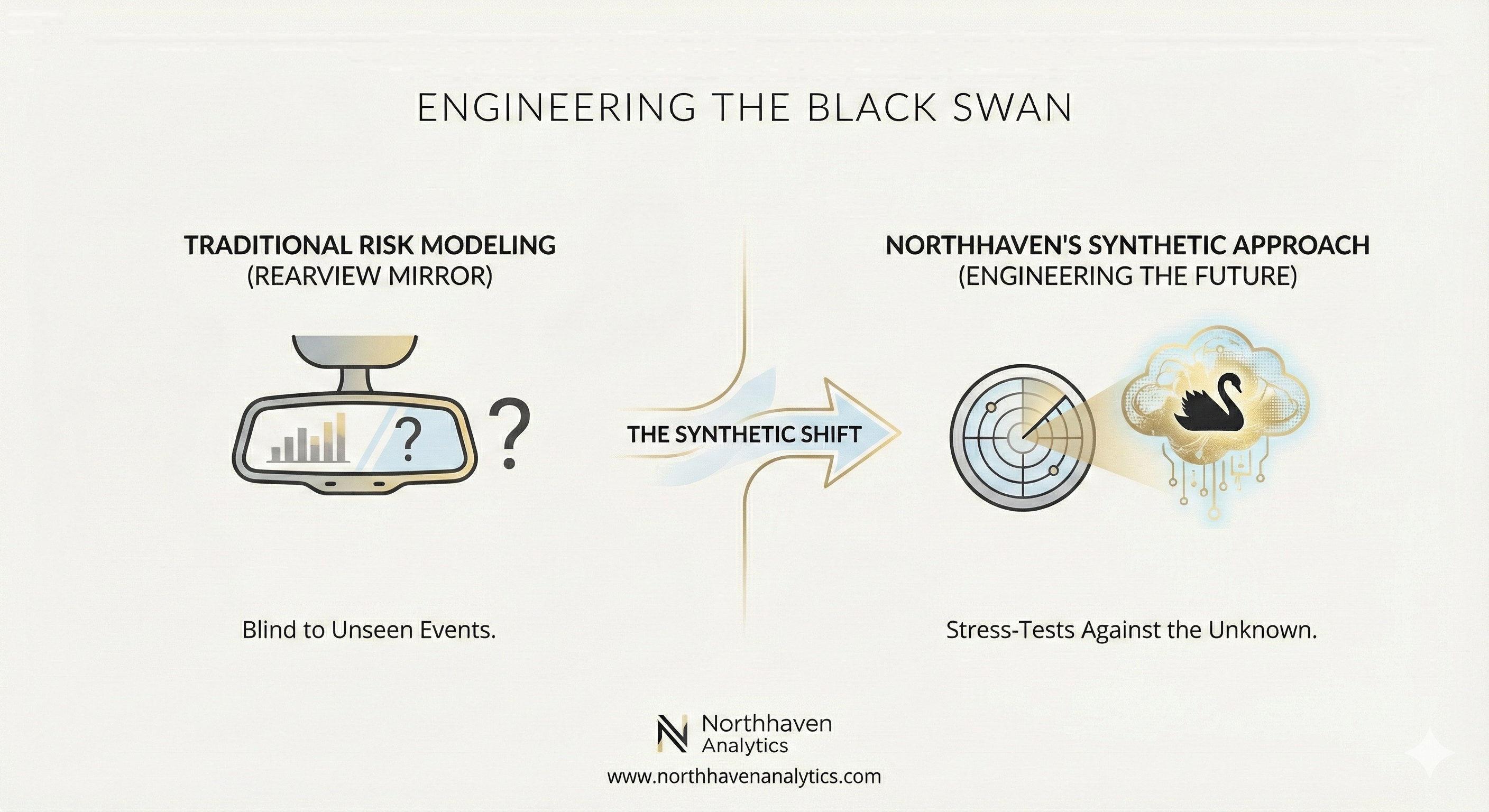

Introduction: The „Rearview Mirror” Problem

In financial risk management, there is a fatal flaw embedded in almost every predictive model: Historical Bias.

Banks and hedge funds train their algorithms on data from the last 5, 10, or 20 years. They look at the 2008 Financial Crisis, the 2020 COVID crash, and the 2022 inflation spike. They teach their models: „This is what risk looks like.”

But the next crash never looks like the last one.

If your risk models are trained solely on historical production data, you are driving a car at 200 km/h while looking exclusively in the rearview mirror. You are blind to the „Black Swans”—the low-probability, high-impact events that have never happened before, until they do.

This is where Synthetic Financial Data becomes a strategic weapon. It is the only technology that allows institutions to engineer the future, rather than just recording the past.

The Trap of Historical Data in Risk Modeling

Traditional Quantitative Risk Management relies heavily on Monte Carlo simulations based on historical covariance matrices. While mathematically sound for normal market conditions, this approach fails during structural breaks.

- Data Scarcity of Tail Events: Real-world financial history doesn’t have enough „apocalypses.” If you are training a Deep Learning model to predict default rates during a 40% currency devaluation, you might have zero data points in your history.

- Overfitting to Stability: Models trained on the „Great Moderation” (periods of low volatility) learn that markets are generally stable. When volatility spikes, these models drift and fail instantly.

To build resilient AI, you need data that represents extreme volatility. Since reality hasn’t provided it yet, you must manufacture it.

Defining Synthetic Financial Data in the Context of Risk

Synthetic Financial Data is often misunderstood as merely a privacy tool. While GDPR compliance is a massive benefit, the true power lies in Data Augmentation.

Through Generative AI (specifically Conditional GANs and Variational Autoencoders), Northhaven Analytics creates datasets that:

- Preserve the Statistical Soul: They maintain the baseline correlations of your portfolio (e.g., the relationship between LTV and Probability of Default).

- Inject Counterfactual Logic: We can mathematically „tilt” the generative model to produce valid financial records under conditions that do not exist in the real world.

We don’t just anonymize your current clients. We generate the clients you would have if the economy collapsed tomorrow.

How It Works: Injecting Shocks into the Latent Space

At Northhaven, we move beyond simple tabular synthesis. We utilize Conditional Generative Adversarial Networks (C-CTGAN) combined with Temporal Sequence Modeling (TSM).

Here is the engineering breakdown of how we simulate a crash:

1. Learning the Latent Manifold

Our model learns the multi-dimensional „shape” of your portfolio. It understands that a high-income borrower usually has a low utilization rate. This is the baseline reality.

2. Conditional Oversampling (The „What-If” Switch)

We intervene in the generation process. We condition the Generator ($G$) to produce records where specific macro-variables shift.

- Command: „Generate 100,000 borrower profiles where

Income_Stabilitydrops by 30% ANDCollateral_Valuedrops by 20% simultaneously.”

3. Generating the Ripple Effect

Unlike Excel-based stress tests, which just lower numbers linearly, our Synthetic Financial Data engine captures the non-linear ripple effects.

- Does a drop in collateral value lead to immediate default, or just higher utilization of credit cards?

- Our TSM architecture generates the behavioral sequence (transactions over 12 months) that results from this shock, providing a realistic view of how liquidity dries up day-by-day.

Regulatory Alignment: Basel IV and SR 11-7

Using Synthetic Financial Data is not just about better math; it is about better compliance.

SR 11-7 (Model Risk Management)

The Federal Reserve and ECB require banks to validate models against „robust stress scenarios.” Using a synthetic dataset that simulates a unique, never-before-seen crisis provides the ultimate evidence of model robustness. It proves your AI isn’t just memorizing history—it actually understands risk.

Capital Efficiency (Basel III/IV)

By demonstrating to regulators that your internal models are robust against extreme synthetic scenarios, institutions can argue for lower Model Uncertainty (MU) buffers. This potentially frees up capital that would otherwise be frozen as a regulatory safeguard.

Case Study: The „Impossible” Inflation Scenario

Consider a Private Debt fund in 2021. Inflation had been low for decades. Their models assumed interest rates would stay near zero. A traditional modeler has no data to train a „High Inflation” AI. Using Northhaven’s engine, the fund generates a Synthetic Financial Data set representing a 1970s-style stagflation environment but applied to 2021 borrower profiles.

- Result: They identify a specific segment of „Prime” borrowers (tech sector employees with high variable equity compensation) who default rapidly when rates hit 5%.

- Action: They adjust their underwriting criteria before the 2022 rate hikes occur, saving millions in defaults.

Conclusion: Stop Predicting, Start Simulating

The era of relying solely on realized historical data is over. In a world of climate change, geopolitical instability, and algorithmic trading, the past is a poor predictor of the future. Synthetic Financial Data allows you to bring the future into the present. It turns Risk Management from a passive reporting function into an active engineering discipline. Don’t wait for the Black Swan to land. Build it in the lab, test your defenses, and survive when others fail. Ready to stress-test your AI infrastructure? Explore our Dedicated Generative Models at www.northhavenanalytics.com.